Disclosure: The author of this story owns shares in MicroStrategy (MSTR).

Shares of self-described Bitcoin Development Company MicroStrategy (MSTR) continue to advance relative to the price of bitcoin (BTC), expanding the premium to the value of its holdings to the highest level in more than three years.

The company’s so-called net asset value (NAV) premium is calculated by dividing MSTR’s market capitalization by the value of its bitcoin stack, and it has risen to roughly 2.5, according to MSTR-tracker, the highest level since February 2021. At current pricing, MicroStrategy has a market cap of around $37.14 billion, with its 252,220 BTC valued at $15.1 billion.

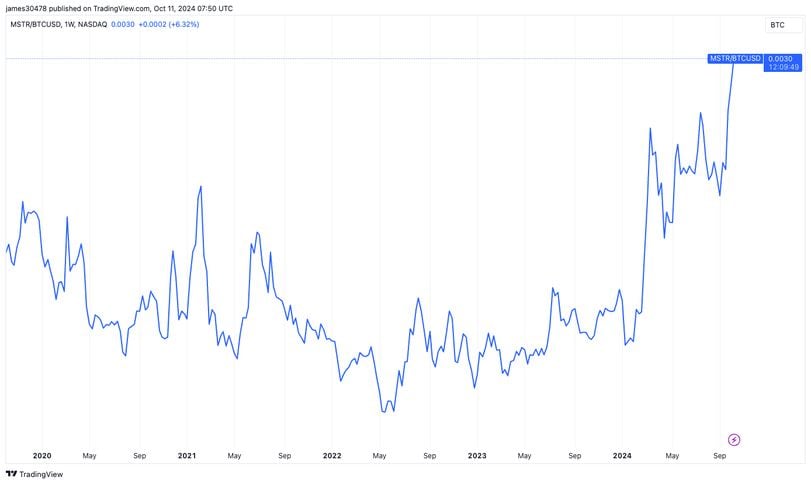

Not only is the NAV multiple at its highest level for years, but dividing the MicroStrategy stock price by the bitcoin price totals 0.0030. That’s the highest ratio since the company’s adoption of bitcoin started in August 2020.

MicroStrategy has outperformed bitcoin in 2024

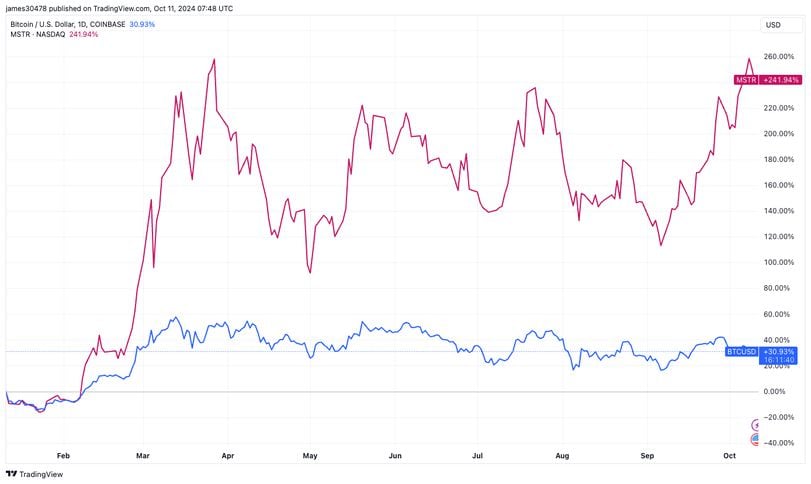

When the spot bitcoin exchange-traded funds launched on Jan. 11, there was much deliberation beforehand about how bitcoin-related equities, such as MicroStrategy, would perform due to the huge expectations of the ETFs.

However, since the launch of the ETFs, MicroStrategy stock has gained more than 240%, making a new record high on Oct. 8. That’s about 8 times better than the performance of bitcoin, which is lower by 16% since hitting its own record all the way back in March.

Explaining the premium

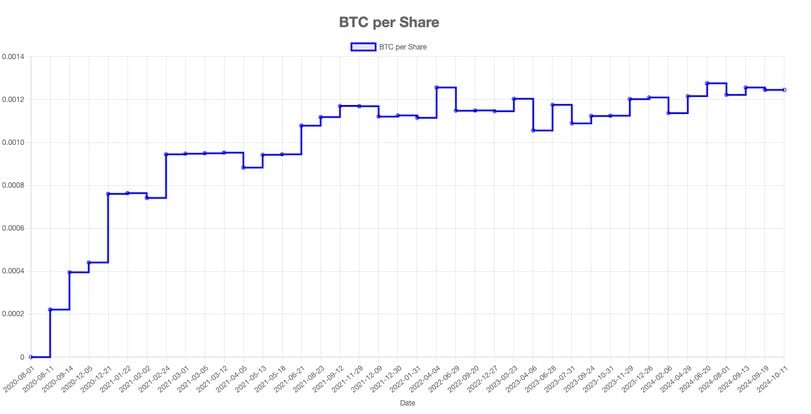

Since adopting bitcoin as a balance sheet asset in August 2020, MicroStrategy has aggressively leveraged financial instruments such as at-the-market equity offerings (ATM) and convertible senior notes to raise capital to steadily boost its coin stash. As a result, the bitcoin per share has continued to increase, which is accretive for shareholders.

Bitcoin per share can be defined as the amount of bitcoin that each outstanding share of MicroStrategy equates to, which is currently at 0.0012.

In both instances, equity financing and debt financing involve shareholder dilution. The share count for debt financing increases once the convertible debt is converted into equity. Meanwhile, equity offerings involve shareholder dilution each time shares are sold through the ATM program. However, the important part is whether the bitcoin holdings can grow faster than the shareholder dilution, and that’s been the case over the last four years.

A new key performance indicator (KPI) coined by MicroStrategy is the “Bitcoin Yield,” which the company defines as the percent change period-to-period of the ratio between the company’s bitcoin holdings and its Assumed Diluted Shares Outstanding.” This metric increased to 5.1% for the second quarter, up from 4.4% three months earlier.

With MicroStrategy showing no signs of stopping this aggressive accumulation strategy and investors seeking greater returns than holding bitcoin itself, the NAV premium could in theory continue over a long period.