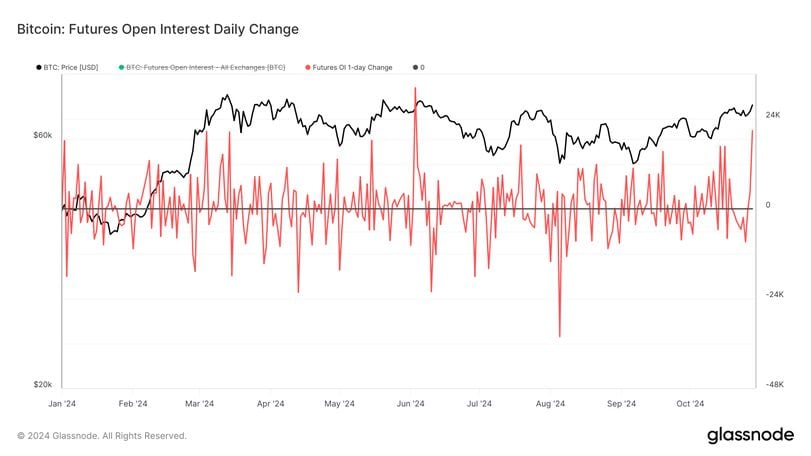

Bitcoin (BTC)-tracked futures set a record high open interest (OI) in U.S. dollar terms early Tuesday as the asset broke past $71,000 for the first time since June, data shows.

BTC futures recorded their biggest one-day jump since June 3 with OI jumping over 20,000 BTC, worth $2.5 billion at current prices, to reach almost 600,000 BTC, or $42.6 billion, as of Tuesday.

OI refers to the total number of outstanding derivative contracts, such as futures or options, that have not been settled. High open interest indicates that there is significant interest in a particular asset. When open interest increases along with rising prices, it suggests new money is coming into the market, indicating a strengthening trend – such as Tuesday’s.

High open interest can lead to increased volatility, especially as contracts near expiration. Traders might rush to close, roll over, or adjust positions, which can lead to significant price movements. Research firm Kaiko said in an X post that while futures showed strong interest from traders, the funding rates for such positions remain well below March highs which indicate tempered demand.

Funding rates in perpetual futures markets are periodic payments made between traders to ensure that the price of the perpetual contract remains close to the spot price of the underlying asset. Traders such as Singapore-based QCP Capital remain bullish on BTC in the near term, expecting price gains to continue in the weeks ahead.

“With rising expectations around a potential Trump victory boosting both stocks and Bitcoin, we believe BTC is well-positioned for medium-term gains,” the firm wrote in a Tuesday broadcast on Telegram.

Reasons why BTC OI has zoomed

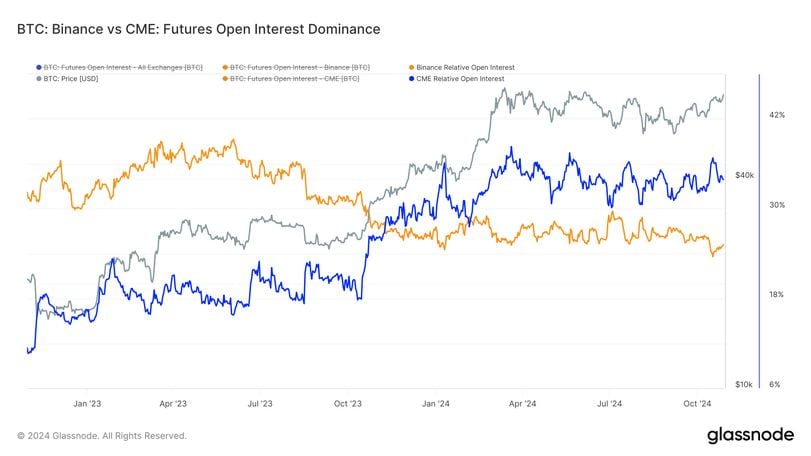

Contracts offered on the Chicago Mercentile Exchange (CME) have seen a 9% surge in 24 hours, taking their open interest to 171,700 BTC, worth over $12.22 billion, which gives CME a 30% dominance in the futures open interest market. As they maintain their number one spot in this market.

In mid-October, bitcoin was trading around $67,000 and the OI on CME hit all-time highs in both notional open interest ($12.4 billion) which is the dollar value of the futures contracts and bitcoin denominated futures contracts (179,930 BTC), per Glassnode data.

Second, the funding rate in perpetual markets has also soared in the past 24 hours to 15%, according to Coinglass data, this is one of the highest recorded levels in the past few months, which shows an extreme bias for bullish long trades.

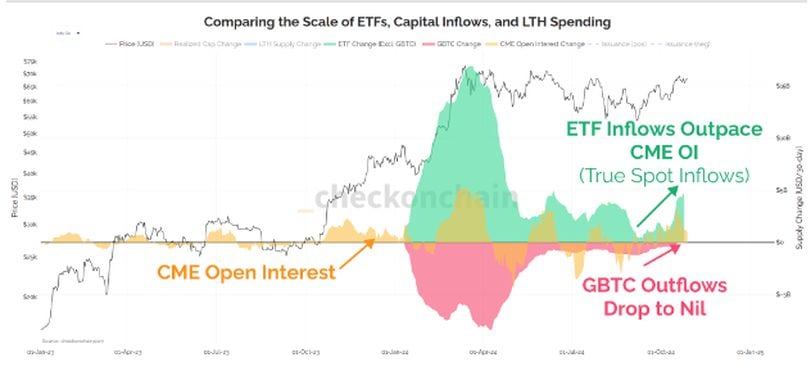

Finally, the third reason can be attributed to the strong inflows from the U.S. listed spot ETFs, which in recent weeks has seen a slight evolution from the institutional basis trade at the start of the year to now more bullish long directional plays.

Since Oct. 16 bitcoin denominated futures contracts peaked on the CME exchange, it has since dropped by over 6%, which has been the opposite for the ETF inflows which have seen a cumulative net inflow of $2.7 billion. The charge has been led by BlackRock’s iShares Bitcoin Trust (IBIT), which has seen $2.2 billion of net inflows in the same time period while achieving a new record of holding over 400,000 bitcoin in the ETF.

Earlier in the year it was apparent that the basis trade or the cash and carry arbitrage was taking place which involves taking advantage of the price difference between the bitcoin spot and futures price. The basis trade involves taking a long position on the ETF and then taking a short position on the CME futures bitcoin price. This was one of the reasons bitcoin has been trading in a long sideways range since March, as not all the inflows from the ETFs were directionally long but overall a net neutral strategy.

Checkmate, an analyst, also noted the recent divergence between the CME OI and the ETF inflows.

“We have a divergence between Bitcoin ETF Inflows and CME Open Interest. ETF Inflows are ticking meaningfully higher. CME Open Interest is up, but not as much. GBTC outflows are also minimal. We’re seeing true directional ETF inflows, and less so cash and carry trades,” Checkmate wrote.

The recent purchase of the Grayscale Bitcoin Mini Trust (BTC) by the Emory University endowment could support Checkmate’s point of view to be a directional long purchase, as one would not expect a University to start executing the basis trade. Emory University would be the first endowment to purchase a bitcoin ETF and while $15 million isn’t a large sum for an institutional investor the narrative and the directional play stand out in a similar fashion to the Wisconsin Pension Fund.

However, Andre Dragosch, head of research at Bitwise, takes the other side of this view: he believes due to the increase in net short-positioning and an increase in CME open interest in the past 24 hours, that the basis trade has already started to pick up, he told CoinDesk in a note.

“There was an increase in net short positioning judging by the change in net non-commercial positioning on CME since early September. This coincided with an overall increase in CME open interest which implies that net there has really been an increase in cash-and-carry trades,” he wrote in a note to CoinDesk. “However, we only have weekly data up to 22/10 from the CFTC, so we don’t have insights into the latest OI change yet”.